Securing optimal capital for a hospitality asset requires navigating a complex web of shifting interest rates, strict underwriting standards, and evolving market dynamics. Investors must deploy sophisticated strategies to maximize their return on investment while mitigating operational risks in a volatile economic climate. This blog will provide a comprehensive guide to Hotel Financing, detailing the essential capital structures and valuation methods needed to successfully secure your next acquisition.

Defining The Fundamentals Of Hospitality Capital

The landscape of hospitality real estate demands specialized capital strategies. Here are the foundational elements that define this complex market.

The Core Mechanics Of Acquiring Lodging Assets

Acquiring a commercial lodging facility is fundamentally different from purchasing traditional real estate assets like multi family apartment buildings or industrial warehouses. Traditional commercial real estate relies on long term leases that guarantee predictable recurring cash flows over several years. In contrast, lodging facilities operate on daily leases, meaning their revenue fluctuates wildly based on seasonality, local market events, and macroeconomic trends.

This inherent volatility makes securing reliable Hotel Financing a highly specialized discipline that requires lenders to possess a deep understanding of daily operational metrics. Lenders must evaluate the physical asset alongside the strength of the business operations running inside it. Therefore, presenting a robust business plan with well projected daily revenues is absolutely critical.

Differentiating Hospitality Real Estate From Traditional Assets

Because lodging revenues reset every single night, lenders view these assets through a distinctly different risk paradigm. A sudden economic downturn can immediately decimate a property’s occupancy rate, whereas an office building with ten year corporate leases might weather the same storm without missing a single rent payment. Consequently, financial institutions demand significantly higher risk premiums when underwriting hospitality loans.

Borrowers must compensate for this perceived risk by providing extensive historical operating data and demonstrating a profound mastery of yield management techniques. Providing detailed competitor analyses and long term demand generation strategies helps alleviate these lender concerns. Investors who prove their operational resilience are far more likely to secure favorable terms.

The Interplay Between Operations And Real Estate Value

The true value of a lodging facility is inextricably linked to the quality of its daily management team. Unlike a passive warehouse investment, a hospitality asset is a living, breathing retail business wrapped inside a real estate shell. If the management team fails to optimize room rates or control labor costs, the net operating income will plummet, directly destroying the underlying real estate value.

Therefore, lenders meticulously scrutinize the track record of the proposed management company before approving any Hotel Financing requests. Operators must clearly illustrate how they intend to capture direct bookings, manage variable costs, and drive total revenue per available room. A premium asset paired with a mediocre management team will quickly lose its financeable equity.

Evaluating Profitability In A Modern Market Context

The macroeconomic environment for hospitality assets has transitioned from an aggressive post pandemic recovery into a period of stabilized normalization. The United States market ended 2025 with a slight 0.3% annual decline in revenue per available room. Looking ahead through 2026, revenue growth is expected to remain modest, generally landing in the 0.5% to 1.0% range.

This stabilized performance is primarily driven by average daily rate increases of 1.0% to 2.0%, which are actively offsetting slight softenings in overall occupancy rates. Investors must base their financial underwriting on these highly realistic market expectations rather than outdated, inflated growth models. Accurate projections protect the asset from dangerous leverage positions down the road.

Hotel Investment: Is It Profitable To Invest In A Lodging Asset?

Maximizing the bottom line is a prerequisite for securing favorable debt terms. Below is a detailed analysis of the metrics driving modern asset profitability.

Revenue Per Available Room Dynamics And Profit Margins

Revenue per available room is the ultimate barometer of a property’s top line health and operational efficiency. However, top line revenue is only half of the profitability equation, as operators must simultaneously battle unprecedented increases in daily operating expenses. Labor remains the most consequential lever in profitability, with the average wage cost per occupied room increasing by 12.8% to reach $48.32.

When labor costs rise faster than top line revenue, severe margin erosion follows quickly, forcing owners to rethink their entire operational strategy. Balancing this equation requires a meticulous focus on lean operations, cross training staff, and aggressively pursuing high margin ancillary revenues. Profitability is entirely achievable when strategic expense control is paired with optimal pricing strategies.

Analyzing The 2026 Global Transaction Volume Rebound

Despite challenges in the broader debt markets, global transaction volumes demonstrated significant momentum recently, posting $24 billion in United States transaction volume alone. Direct investment rose by 22% from previous troughs, signaling a renewed institutional appetite for yield generating assets. Improved debt market conditions have enabled a return of larger scale transactions exceeding $250 million.

Cross border capital flows are also accelerating as international investors seek diversification in premium urban markets. As institutional capital returns to the hospitality sector, independent sponsors must remain agile to successfully compete for prime acquisitions. This resurgence proves that lodging assets remain a highly attractive asset class for diversified commercial portfolios.

The Impact Of Artificial Intelligence On Operating Expenses

Artificial intelligence is fundamentally reshaping how properties manage their most expensive operational line items to protect their debt service coverage ratios. Advanced pricing algorithms analyze competitor rates, local market events, and real time booking paces to optimize daily room rates automatically. Early adopters of these dynamic pricing systems have reported massive revenue per available room increases of up to 15%.

Furthermore, predictive maintenance sensors are minimizing equipment downtime by 40%, directly insulating the property’s bottom line from unexpected capital expenditures. By integrating advanced technology into daily operations, properties can significantly reduce human error and minimize wasted labor hours. These technological efficiencies make the asset infinitely more attractive to conservative commercial lenders.

Driving Direct Bookings To Boost Net Operating Income

Online travel agencies provide massive global visibility, but their exorbitant commission structures heavily dilute a property’s net operating profit. Standard commission rates often range from 10% to over 25% of the total booking value, creating a significant drag on overall profitability. Shifting the revenue mix toward direct bookings eliminates these third party fees, allowing the operator to capture a vastly higher percentage of the gross revenue.

Because Hotel Financing constraints are intrinsically tied to net operating income, every dollar saved on commissions exponentially increases the building’s financeable asset value. Executing a highly optimized direct booking strategy is an absolute necessity for protecting property margins in a competitive market. Engaging digital marketing experts is a direct pathway to significantly boosting the final valuation of the asset.

The Vietnam Market As An Emerging Profitability Case Study

While established Western markets offer stability, emerging markets like Vietnam are demonstrating remarkable resilience and recovery momentum. Vietnam welcomed 19.1 million international tourists recently, representing a massive 20.9% year over year increase. Occupancy rates have climbed significantly, driven by a renewed influx of Asian and European source markets.

Real estate experts project that transaction volumes in Vietnam could reach $200 million in 2026 if sufficient institutional grade assets enter the market. Before pursuing complex cross border acquisitions or domestic value add projects, investors must ensure their business plan is financially sound and optimized for maximum operational profitability. Understanding local nuances and regional growth indicators guarantees a much safer international capital deployment.

The Mechanics Of Capital: How Does Hotel Funding Work Today?

Building a resilient capital stack is the most critical component of any lodging acquisition. Let us explore the specific debt and equity instruments utilized by institutional sponsors.

Building The Traditional Capital Stack

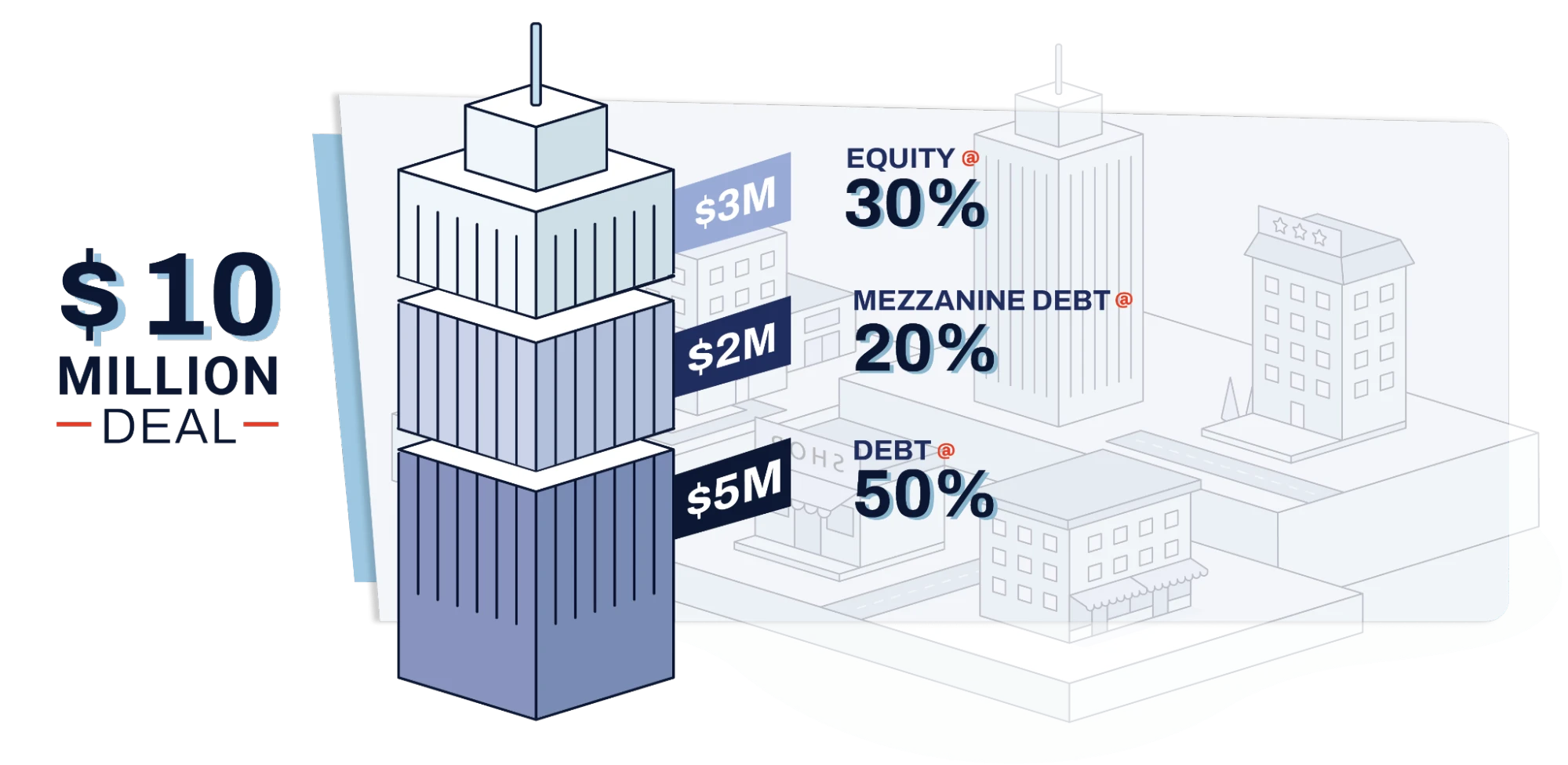

The traditional capital stack is a hierarchical structure of financing that dictates the exact order of repayment and risk assumption. Senior debt forms the foundational baseline, holding the absolute first priority of payment in the event of a liquidation or default. This primary mortgage usually comprises 50% to 70% of the total capital stack and commands the lowest interest rates, generally yielding 5% to 8% for the lender.

Common equity sits at the very top of the stack, absorbing the highest amount of risk but capturing all of the residual upside and profit. Between the senior debt and common equity, sponsors frequently layer subordinate debt to complete the required funding. Properly structuring these layers ensures the project is fully capitalized without overburdening the daily cash flow.

Understanding Debt Service Coverage Ratios And Covenants

Lenders utilize the debt service coverage ratio to determine a property’s ability to comfortably manage its monthly mortgage obligations. This critical metric is calculated by dividing the property’s annual net operating income by its total annual debt service. In the current economic climate, institutional lenders are enforcing incredibly strict underwriting standards to protect their downside risk.

Most commercial banks and life insurance companies are demanding debt service coverage ratios between 1.30x and 1.35x, ensuring robust cash flow cushions. Failing to maintain these strict covenants can trigger severe default provisions or force the property into expensive cash management lockboxes. Accurate financial projections are essential for convincing lenders that the property will easily clear these rigorous coverage hurdles.

The Role Of Loan To Value And Debt Yield Metrics

While loan to value ratios were once the primary driver of commercial lending, modern underwriters are placing unprecedented emphasis on the debt yield metric. The debt yield is calculated by dividing the property’s net operating income by the total loan amount, providing a clear picture of the lender’s cash on cash return if they were forced to foreclose.

Top tier lenders currently require a stabilized debt yield of 10.5% to 12.0% for premium assets. Consequently, loan to value maximums have compressed significantly, with most conservative lenders capping their exposure at 60% to 65% of the appraised value. Understanding how lenders weigh these metrics allows sponsors to accurately determine exactly how much equity they need to bring to the closing table.

Navigating The Pre Development And Soft Costs Landscape

When structuring construction loans, developers must carefully account for soft costs, which often catch inexperienced sponsors off guard. Soft costs encompass entitlement fees, architectural designs, environmental permits, franchise application fees, and legal due diligence. Financing costs and carrying costs during the extended pre development period represent the largest component of this category.

In highly regulated urban markets, securing these initial entitlements can take years, requiring significant upfront equity before any senior debt can be drawn down. Developers who fail to allocate sufficient capital for these soft costs frequently find their projects stalled before ground is even broken. A meticulously planned pre development budget is absolutely vital for keeping the project timeline intact.

Property Improvement Plans And Their Financial Burden

When purchasing a branded property or renewing a franchise agreement, owners are universally required to execute a property improvement plan. These mandated renovations ensure the physical asset aligns with current brand standards regarding technology, furnishings, and life safety systems. The cost of these improvement plans varies drastically based on the property tier and its existing physical condition. Accurate Hotel Financing models must incorporate these massive capital expenditures to avoid devastating equity shortfalls post closing.

Table 1.1. Expected Property Improvement Costs

| Asset Classification | Average Cost Per Room | Typical Renovation Scope |

| Economy or Midscale | $3,500 to $7,000 | Basic lighting, durable casegoods, standard framed art |

| Upscale or Select Service | $7,500 to $15,000 | Premium finishes, upgraded seating, decorative mirrors |

| Luxury or Full Service | $16,000 to $35,000+ | Custom veneers, bespoke fixtures, designer soft goods |

Valuation Methodologies Decoded For Hospitality Investors

Determining the precise market value of an operating asset requires specialized appraisal techniques. Consider the following methodologies that industry experts deploy to underwrite property values.

Unpacking The Income Capitalization Approach

The income capitalization approach is widely considered the most accurate method for valuing income producing commercial assets. This methodology is based on the fundamental economic principle that the present value of a property is dictated by its future net returns. Appraisers meticulously forecast the property’s future income and expenses, deriving an anticipated earnings stream over a specific holding period.

Because hospitality businesses generate daily revenue, their value cannot be reduced to merely the physical building or the underlying land. This method rigorously analyzes how efficiently the management team converts gross revenues into tangible operating profit. Lenders heavily rely on this specific approach to determine the maximum loan amount they can safely extend to the borrower.

Calculating The Capitalization Rate In A Volatile Market

Capitalization rates act as an inverse measure of perceived market risk, directly translating net operating income into a total asset value. The formula is incredibly straightforward, as the property value equals the net operating income divided by the capitalization rate. In the United States, average hospitality capitalization rates rose to approximately 8% recently, reflecting higher capital costs and a demand for increased risk premiums.

However, prime urban luxury assets in stabilized markets continue to trade at much tighter capitalization rates in the 6% to 7% range. Fluctuating interest rates directly impact these capitalization figures, heavily shifting the final appraised value of the property. Sponsors must closely monitor federal reserve policies to anticipate exactly how these market shifts will affect their exit valuations.

Applying The Summation Method For Asset Breakdown

The cost approach, frequently referred to in appraisal circles as the summation method, estimates a property’s value by calculating the current cost to replace the physical structure. The formula adds the value of the raw land to the construction costs of the improvements, and then subtracts all forms of physical, functional, and economic depreciation.

A key advantage of the summation method is its ability to isolate the value of the physical real estate by systematically stripping away business enterprise value. This isolation makes the summation method highly relevant for property tax appeals, where owners only want to be taxed on the physical real estate rather than their operational success. While rarely used as the primary valuation tool for transactions, it serves as an excellent secondary check against the income approach.

Utilizing The Discounted Cash Flow Model For Long Term Projections

For complex assets with shifting revenue dynamics, the discounted cash flow model provides the most granular valuation framework. This process projects the property’s net operating income over a standard holding period, which is typically ten years. Appraisers then forecast the asset’s terminal value at the end of the holding period by applying an exit capitalization rate to the final year’s projected income.

Both the annual cash flows and the massive terminal value are then discounted back to their present value using a carefully selected risk adjusted discount rate. This comprehensive model accounts for significant planned renovations, brand conversions, and anticipated shifts in future market supply. It offers the most holistic view of an asset’s true financial potential over a long term investment horizon.

Adjusting Multipliers For Age And Market Conditions

A quicker, though less precise, valuation tool is the room revenue multiplier method. Using this technique, the total value of a property is calculated by multiplying its annual rooms revenue by a market derived metric. However, similar to capitalization rates, these multipliers must be heavily adjusted to account for the specific nuances of the subject property.

If a derived multiplier comes from the sale of a newly constructed property, a significant downward adjustment must be applied when valuing a twenty year old asset. While helpful for rapid initial assessments, multipliers lack the depth required for securing serious institutional financing. Thorough financial modeling and deep operational analysis are always required to solidify a truly competitive lending package.

Exploring Options When It Comes To Hospitality Lenders

The lending environment has fragmented into several highly specialized institutional categories. Examine the diverse profile of capital providers currently funding commercial lodging transactions.

Traditional Commercial Banks And Their Underwriting Standards

Local and regional commercial banks remain a primary source of capital for stabilized assets with proven historical performance. These institutions typically offer the most competitive interest rates, often hovering around the 6.75% mark for top quality borrowers. However, traditional banks are highly risk averse and generally cap their leverage at a conservative 55% to 65% loan to cost ratio.

Furthermore, they frequently require the borrower to establish a significant depository relationship, mandating that 10% to 20% of the loan amount be held in accounts at the bank. Sponsors must demonstrate a flawless track record and provide impeccable personal financial statements to secure this highly coveted traditional capital. Commercial banks represent the most affordable, yet the most difficult to obtain, tier of Hotel Financing available today.

Life Insurance Companies Securing Premium Assets

Life insurance companies represent the pinnacle of conservative, long term commercial lending. These massive institutions are aggressively seeking to deploy capital into high quality, stabilized hospitality assets to match their long term liability profiles. Life companies typically offer incredibly attractive interest rates in the 6% to 7% range and frequently structure their loans as non recourse facilities.

To secure these exceptional terms, borrowers must present pristine assets that generate massive cash flow, as life companies prefer highly conservative debt yields of 14% to 15%. They generally focus exclusively on primary urban markets or elite luxury resort destinations with deeply entrenched barriers to entry. Partnering with a life insurance company ensures a highly stable, low cost capital structure for long term asset holds.

Commercial Mortgage Backed Securities And The Maturity Wall

The commercial mortgage backed securities sector is a massive driver of liquidity, pooling individual loans into tradable bonds sold to global investors. These lenders are highly active, offering competitive rates and higher leverage than life companies, provided the asset hits a 13.5% debt yield. However, the sector is currently facing a historic crisis, with approximately $875 billion in commercial real estate debt maturing in 2026 alone.

Within that staggering figure, there are $76.6 billion in hard maturities where borrowers have exhausted all extension options and must refinance immediately. This upcoming maturity wall is forcing many owners to aggressively seek alternative funding options to prevent imminent foreclosure. Navigating the CMBS market requires an experienced advisory team to structure the loan efficiently prior to securitization.

Private Credit And Debt Funds Filling The Capital Void

As traditional banks tighten their lending parameters in response to regulatory pressures, private credit and debt funds have surged to fill the void. The global private credit market reached $238 billion recently, fueled by high net worth individuals and institutional investors seeking robust yields. These agile lenders are highly bullish on transitional hospitality assets, routinely offering leverage up to 70% for value add business plans.

Because they assume greater risk, debt funds price their floating rate loans significantly higher, typically ranging around 10% or priced at SOFR plus 350 to 600 basis points. They provide critical bridge capital for sponsors looking to completely renovate or rebrand a struggling property before stabilizing the asset. While expensive, debt funds offer incredible flexibility and speed of execution compared to heavily regulated traditional banks.

Strategic Refinancing Approaches Amidst Maturity Pressures

The tactic of extending and amending troubled loans is experiencing severe fatigue as lenders face intense pressure to clean up their balance sheets. Properties that have suffered net operating income declines will face significant equity shortfalls when attempting to replace their legacy debt. In response to these harsh conditions, owners are pursuing strategic partnerships with experienced operators to fundamentally reposition their assets.

Successfully navigating this maturity wall requires securing aggressive new Hotel Financing structures that can bridge the valuation gap until interest rates normalize further. Sponsors must aggressively drive top line revenues and ruthlessly cut expenses to make their assets attractive to new lenders. Executing a highly profitable direct booking strategy is the fastest way to artificially inflate the property’s net operating income prior to refinancing.

Alternative Hotel Funding Sources And Structural Options

Beyond primary mortgages, sponsors frequently require creative subordinate debt to bridge equity gaps. Review these alternative funding structures that provide critical leverage in tight credit markets.

The Resurgence Of Mezzanine Debt Instruments

Mezzanine financing sits directly above senior debt and serves to bridge the critical gap between primary mortgages and sponsor equity. Instead of placing a traditional mortgage lien on the physical real estate, mezzanine lenders secure their capital by placing a lien on the ownership shares of the entity that owns the property. If a default occurs, the mezzanine lender can execute a rapid foreclosure on the entity shares, effectively taking total control of the asset.

Because of this elevated risk position and lack of hard collateral, mezzanine debt commands higher interest rates, often ranging from 10% to 20%. Despite the steep cost, this financing layer is incredibly valuable for sponsors who lack the total liquid equity required to close a massive acquisition. Mezzanine loans allow skilled operators to safely acquire premium properties and execute high yield business plans.

Structuring Preferred Equity For Subordinate Capital

Preferred equity represents an ownership stake in the property entity rather than a traditional creditor loan. This layer of the capital stack provides priority distributions over common equity holders, typically targeting a preferred return of 8% to 12%. Unlike mezzanine lenders, preferred equity investors are unsecured and do not have traditional foreclosure rights, though they may secure the right to replace management.

Many sponsors favor preferred equity in modern Hotel Financing because it often circumvents the strict additional indebtedness clauses found in senior commercial mortgage documents. It functions as a highly flexible hybrid tool, offering characteristics of both standard equity and structured debt. Carefully incorporating preferred equity into the capital stack allows developers to maximize their own personal returns upon the final sale of the asset.

Government Backed Small Business Administration Loans

The Small Business Administration provides highly attractive lending programs designed specifically for independent operators and franchise owners. These government backed initiatives significantly reduce the risk for participating conventional lenders, allowing borrowers to access capital with lower down payments. The two primary vehicles utilized in the hospitality sector are the standard 7(a) program and the real estate focused 504 program. Both programs have strict eligibility requirements, mandating that the business operates for profit and falls within specific revenue size standards.

Table 1.2. Small Business Administration Lending Parameters

| Lending Parameter | SBA 7(a) Loan Program | SBA 504 Loan Program |

| Maximum Loan Size | Up to $5 Million | Up to $30 Million |

| Interest Rate Structure | Predominantly Variable | Fixed Rates |

| Current Rate Range | 9.75% to 14.75% | 5.00% to 7.00% |

| Primary Use Case | Acquisitions, Working Capital | Real Estate, Heavy Construction |

| CDC Involvement | Not Required | Strictly Required |

Commercial Property Assessed Clean Energy Financing

Commercial Property Assessed Clean Energy funding has evolved from a niche sustainability product into a mainstream capital solution. This financing mechanism provides long term, low cost capital for energy efficiency, water conservation, and structural resiliency upgrades. The loans are repaid through a voluntary tax assessment on the property, allowing the debt to amortize over terms as long as 20 to 30 years.

Recent legislative changes, such as Florida completely eliminating its previous 3.5 year lookback restriction, have massively expanded how developers can utilize these funds to strengthen their capital stacks. C-PACE funding frequently replaces highly expensive mezzanine debt, significantly lowering the overall blended cost of capital for new developments. It is an exceptionally strategic financial tool for sponsors prioritizing eco friendly and sustainable building practices.

Utilizing Ground Leases For Capital Efficiency

A ground lease is a highly complex real estate transaction where the ownership of the physical improvements is legally separated from the ownership of the underlying land. Under this structure, a tenant leases the raw land for an extended period, often 50 to 99 years, and constructs a lodging facility at their own expense. This strategy allows developers to drastically reduce their initial upfront capital requirements since they do not need to purchase the expensive urban land.

Structuring these diverse layers without violating senior loan covenants is a delicate process that requires extreme financial proficiency. Separating the land ownership creates an incredibly efficient capital structure, heavily boosting the sponsor’s final cash on cash returns. Mastering this specialized mechanism opens the door to prime urban developments that would otherwise be entirely cost prohibitive.

Best Practices For Navigating A Hospitality Transaction

Successfully closing a transaction requires meticulous preparation and proactive risk management. Analyze the essential strategies that protect developers from unforeseen liabilities.

Compiling A Bulletproof Due Diligence Checklist

The due diligence period is the most critical phase of any acquisition, allowing the buyer to thoroughly verify all physical and financial representations made by the seller. A comprehensive Hotel Financing checklist must include three years of detailed income and expense statements, complete with monthly operational figures. Buyers must also secure comprehensive property surveys, environmental impact reports, and a summary of all existing commercial leases.

Furthermore, lenders will demand extensive biographical background information on every managing partner to verify their industry experience before approving funds. Incomplete due diligence frequently leads to massive post closing financial surprises, fundamentally destroying the anticipated profitability of the deal. Securing a highly competent advisory team ensures that no hidden liabilities are overlooked during this extremely sensitive review phase.

Avoiding Common Missteps In Business Planning

Many promising lodging projects fail entirely due to a lack of proper financial planning and proactive risk management. One of the most common pitfalls is over leveraging the asset during the acquisition phase, leaving the property with zero margin for error if revenues decline. Conversely, under capitalizing a project by failing to raise sufficient working capital will quickly paralyze operations during the turbulent pre opening phase.

Sponsors must maintain a highly disciplined approach to their capital structure, ensuring that their amortization schedules align perfectly with their projected cash flow ramps. Optimism must always be balanced with strict financial conservatism when forecasting future occupancy levels and average daily rates. Presenting a rigorously tested, data backed business plan is the only way to successfully secure funding from top tier institutional lenders.

Underestimating Operational Costs And Risk Factors

When underwriting a potential acquisition, inexperienced buyers frequently underestimate the creeping rise of fixed operational expenses. Property insurance premiums and local property taxes have skyrocketed across the nation, severely compressing historical profit margins. Additionally, the sheer cost of maintaining a specialized hospitality workforce requires constant vigilance and aggressive recruitment strategies.

If an underwriter relies entirely on historical expense data without projecting these aggressive future increases, the entire financial model will collapse within the first year of operations. Sophisticated sponsors build robust contingency buffers directly into their financial projections to absorb these inevitable economic shocks. Accurate cost forecasting proves to the lender that the sponsor possesses a profound understanding of modern hospitality operations.

Aligning Capital Partners With Long Term Vision

Selecting the right capital partner is just as important as negotiating the specific interest rate on the loan facility. Entrepreneurial sponsors executing heavy value add renovations need flexible, patient capital that understands the inevitable delays associated with construction projects. If a sponsor pairs a volatile repositioning strategy with an inflexible, highly regulated institutional lender, technical defaults are almost guaranteed to occur.

The operating agreement and intercreditor documents must clearly define exactly how cost overruns and timeline extensions will be handled between all equity and debt partners. Securing alignment from day one prevents highly destructive legal battles if the project deviates slightly from the initial business plan. Establishing clear communication and trust with your lending partners ensures a smooth, highly cooperative execution phase.

Stress Testing The Asset Against Economic Volatility

Before finalizing any capital commitments, the acquisition model must be rigorously stress tested against severe macroeconomic shocks. Analysts should run sensitivity models that simulate a sudden 20% drop in average daily rates or a massive spike in baseline interest rates. This exercise reveals exactly when the debt service coverage ratio will break, allowing the sponsor to pre fund appropriate interest reserves.

Proactive risk management is the absolute defining characteristic of elite institutional investors who consistently generate outsized returns regardless of broader market conditions. By explicitly showing the lender exactly how the property will survive an economic downturn, sponsors build immense operational credibility. A stress tested asset is a secure asset, heavily driving the ultimate likelihood of a successful loan approval.

Conclusion

The landscape of commercial real estate has become highly sophisticated, demanding that investors master capital stacks, alternative lending options, and strict debt coverage ratios. Whether you are executing a heavy value add repositioning or looking to refinance a stabilized luxury asset, securing the optimal cost of capital is your ultimate driver of long term wealth creation. By fully understanding the fundamental shifts in lending requirements and preparing robust financial models, you can safely navigate today’s volatile markets and close your acquisitions successfully.

Ready to maximize your return on investment? Successfully acquiring and scaling a hospitality asset requires expert financial planning and aggressive digital growth strategies. Partner with the hospitality performance marketing professionals at ROI300 to build, automate, and scale your direct bookings, significantly boosting your Net Operating Income to secure much better lending terms. Contact ROI300 today to elevate your asset’s valuation and completely dominate your target market.